.jpg) Niels Buksik

Niels Buksik

What Can You Buy With 529 Distribution?

The biggest challenge for students and parents when planning for education are the financial costs; including tuition and academic expenses. It’s not...

Have questions about the recent student loan forgiveness announcement?

I’ve got (some) answers.

(Please forward this email to anyone you know who might need some clarity about their student loans. There's also a very important note about scams at the bottom that's worth sharing. #themoreyouknow)

You've probably heard by now that the government plans to forgive federal student loans for roughly 20 million Americans.1

Here's what we know about the loan forgiveness so far:2

The student loan payment moratorium is also extended through December 31, 2022. This means payments start on your new balance on January 1, 2023.

But! Here's a big detail that got left out of most headlines:

Under new Dept. of Education rules, monthly payments on undergraduate debt will be slashed to 5% of a borrower's "discretionary income," and the amount of income shielded from repayment calculations will also increase.3

This rule change could end up halving monthly payments for millions of folks and might be an even bigger deal than one-time forgiveness.

Will I owe taxes on the forgiven loan amount?

It depends. While you would typically owe federal taxes on forgiven debt, the American Rescue Plan exempted student loans from the usual federal tax rules.4

Many states have decided not to levy state taxes, but some states explicitly will or haven't announced their position. Depending on where you file state income taxes, you may owe taxes.

What if I made loan payments during the moratorium? Can I get a refund?

Very likely. Any payments on your qualifying federal loans made since March 13, 2020 can be refunded by contacting your loan servicer.5

How do I get my loans (or my kids' loans) forgiven?

According to the Dept. of Education, an online application will be available by October, and you'll have until December 31, 2023 to apply.2

Those who filled out FAFSA forms in 2021-2022 for themselves or their dependent children may be automatically enrolled in the forgiveness program because their relevant income information is already on file.6

How big a deal is this whole thing, economically speaking?

Hard to say yet. Court challenges or administrative hurdles could change what actually happens and for whom.

Some folks think that forgiving student loans is a bad idea.

The thing is, the federal government has forgiven loans for defrauded students, small businesses, farms, and public service employees for years, so those concerns are probably overblown.

Goldman Sachs economists ran some numbers on the expected effect of the current plan on the economy; they concluded that it probably won't have much macro impact at all, though the caps on monthly payments should increase household income.7

Should I take out more loans so they'll be forgiven?

Please don't. So far, only loans initially disbursed by June 30, 2022 will be covered by this plan. Anything taken out afterward will not be eligible.6

What do I need to do right now?

Nothing. Nada. Zilch. The details are still being hammered out and more information will be coming. A great place to get alerts is from the Dept. of Education. You can sign up for them here.

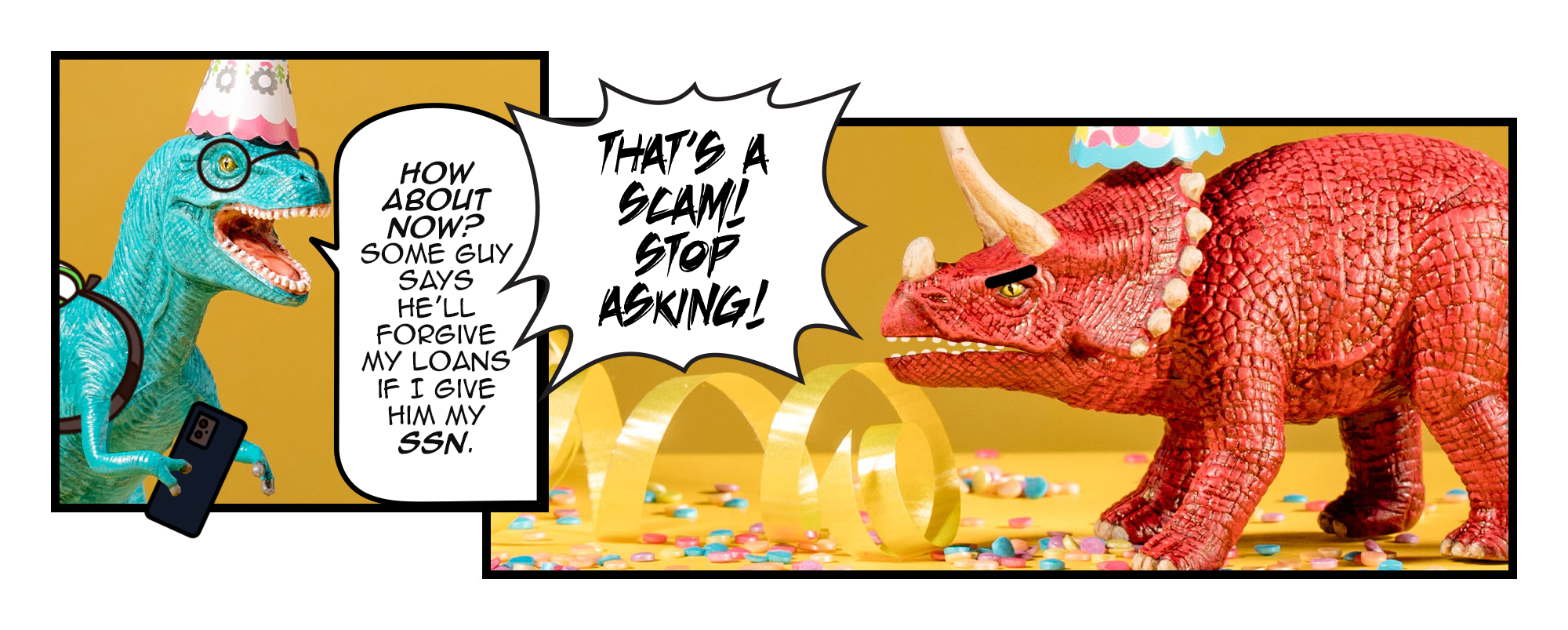

SCAM ALERT: We're expecting A LOT of scammer activity targeting folks waiting for student loan relief. Please be VERY careful with emails or text messages claiming to be about your loans.

Get your information straight from reliable sources like the Dept. of Education and your student loan servicer’s official website (and me!).

If you've read all the way through, thanks for sticking with me. I know this was a lot of information all at once.

We'll know more about the details of the plan in the weeks ahead, but if you have questions or want to update your strategies in anticipation of lower (or no) student loan payments, please hit “reply” to this email and we’ll set up a time.

Scholastically,

Niels Buksik

1 - https://www.cnbc.com/select/biden-to-erase-up-to-20k-in-student-loan-debt-heres-who-qualifies/

2 - https://studentaid.gov/debt-relief-announcement/one-time-cancellation

4 - https://taxfoundation.org/student-loan-debt-cancelation-tax-treatment/

8 - https://finance.yahoo.com/news/stock-market-tanked-since-jerome-211327050.html

Risk Disclosure: Investing involves risk including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values. Past performance does not guarantee future results.

This material is for information purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. The content is developed from sources believed to be providing accurate information; no warranty, expressed or implied, is made regarding accuracy, adequacy, completeness, legality, reliability or usefulness of any information. Consult your financial professional before making any investment decision. For illustrative use only.

Hightower Advisors do not provide tax or legal advice. This material was not intended or written to be used or presented to any entity as tax advice or tax information. Tax laws vary based on the client’s individual circumstances and can change at any time without notice. Clients are urged to consult their tax or legal advisor for any related questions.

This email and any files transmitted with it are confidential and intended solely for the use of the individual or entity to whom they are addressed. If you have received this email in error please notify the system manager. This message contains confidential information and is intended only for the individual named. If you are not the named addressee you should not disseminate, distribute or copy this e-mail. Please notify the sender immediately by e-mail if you have received this e-mail by mistake and delete this e-mail from your system. If you are not the intended recipient you are notified that disclosing, copying, distributing or taking any action in reliance on the contents of this information is strictly prohibited. ANCHORY LLC is an Investment Adviser registered with the Securities and Exchange Commission of Texas. All views, expressions, and opinions included in this communication are subject to change. This communication is not intended as an offer or solicitation to buy, hold or sell any financial instrument or investment advisory services. Any information provided has been obtained from sources considered reliable, but we do not guarantee the accuracy or the completeness of any description of securities, markets or developments mentioned. We may, from time to time, have a position in the securities mentioned and may execute transactions that may not be consistent with this communication's conclusions. Please contact us at 817-203-7325 if there is any change in your financial situation, needs, goals or objectives, or if you wish to initiate any restrictions on the management of the account or modify existing restrictions. Additionally, we recommend you compare any account reports from ANCHORY with the account statements from your Custodian. Please notify us if you do not receive statements from your Custodian on at least a quarterly basis. Our current disclosure brochure, Form ADV Part 2, is available for your review upon request, and on our website, www.anchory.com. This disclosure brochure, or a summary of material changes made, is also provided to our clients on an annual basis.

The biggest challenge for students and parents when planning for education are the financial costs; including tuition and academic expenses. It’s not...

.png)

Certified Financial Planners (CFP®) are professional financial advisors who have met certain education, experience, and ethical requirements set by...

%20(2).png)

Meeting with a financial advisor can be a daunting task, especially if you're not sure what to expect or how to prepare. But with a little bit of...